Chargebacks

When a consumer pays for a Catch purchase with a debit card, they have the option to file a chargeback with their bank. A consumer may file a chargeback if something goes wrong with their order, such as:

- They never received the product

- The product wasn't as described

- They returned the product but did not receive a refund

When a consumer files a chargeback, their bank will notify Catch. Catch will then notify you, and you will decide whether to accept the chargeback as justified or dispute it.

Fraud Protection

Some chargebacks may happen because a stolen debit card was used to make the purchase. In this case, the cardholder will file a chargeback due to fraud.

Catch assumes responsibility for all fraud and covers the cost of these types of chargebacks.

Disputes

While many chargebacks are initiated for valid reasons, consumers sometimes file chargebacks for invalid reasons, such as buyer’s remorse, a desire to return fees, or attempting to receive an item for free. When this happens, Catch will help you collect evidence and present it to the consumer's bank and card network. The consumer's bank is ultimately responsible for deciding which party, you or the consumer, wins the chargeback dispute.

Avoiding Lost Disputes

Before collecting and submitting evidence to dispute a chargeback, we strongly recommend that you try to get in touch with the consumer first to figure out the problem. If you can resolve the problem directly with the consumer, then you should tell the consumer to contact their bank and drop the chargeback. You should also include evidence that the consumer agreed to drop the chargeback in your response to Catch's chargeback notification.

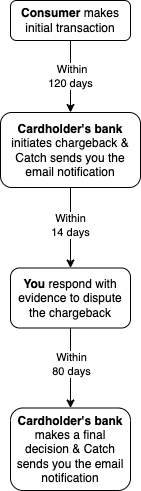

Process Overview

This is the typical process for a chargeback:

- The cardholder files a chargeback with their bank.

- The cardholder's bank initiates the chargeback and notifies Catch.

- If the chargeback is for a reason that is not covered by Catch (see Dispute Reasons & Evidence Collection), the disputed amount is removed from your next payout.

- Catch sends you an email notification with information about the chargeback and a request for evidence to dispute the chargeback, if you don't believe it's justified. You either:

- Accept the chargeback as justified, or

- Respond to the email with the required evidence to prove that the charge was valid.

- If you accept the chargeback or fail to respond to the email within 14 days, Catch will not dispute the chargeback. At this point, the process is over and the disputed amount will not be returned to you.

- If you respond with evidence, Catch will use that evidence to construct a case to the bank to dispute the chargeback.

- The bank reviews the evidence and decides whether you or the consumer wins the dispute. Catch sends you an email notification with this final decision.

- If the consumer wins the dispute, the disputed amount is not returned to you and you are charged an additional $15 fee, which is removed from your next payout.

- If you win the dispute, the disputed amount is returned to you in your next payout.

Avoiding Fees

If you know you're not likely to win a dispute, you should accept the chargeback in order to avoid the additional chargeback fee for a lost dispute.

Timeline